Providing Expert R&D Tax Credit advice. We Combine Technical & Financial Expertise to Identify & Maximise your Innovation & Research & Development Tax Credit Opportunities Across Ireland.

Providing Expert R&D Tax Credits advice. We Combined Technical & Financial Expertise to Identify & Maximise your Innovation & Research & Development Tax Credit Opportunities Across Ireland.

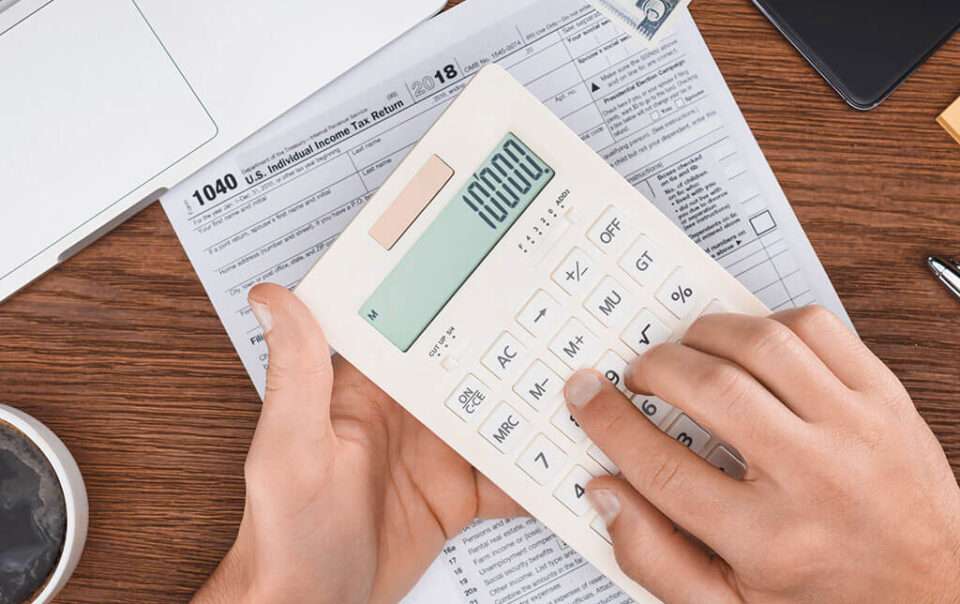

Combined Technical & Financial Expertise to Identify & Maximise your Innovation & R&D Tax Credits Opportunities Across Ireland

Labour and expenditures will determine your next SR&ED Claim

Tailored R&D Tax Credits

Maximise Your Next R&D Tax Credits By 5%-20%

Braithwaite's tailored services increase R&D tax claim amounts, lowers time spent on R&D Technical Report writing and allows our customers to use their time wisely on their Research and Innovation.

We use necessary cookies to enable you to move around our website and use its features. You may disable these by changing your browser settings, but this may affect how our website functions.

We would also like to set optional analytics cookies to help us improve our website by collecting and reporting information on how you use it. However, we will not set these cookies unless you enable them by using the on/off tool below and click the save and close button. Using this tool will set a cookie on your device to remember your preferences.

For more detailed information about the cookies we use, see our Read More You can give or withdraw your consent at any time by clicking the ‘C’ icon at the bottom left of the website.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.